Something you need to know: Some of you might ask what is OPR 马来西亚隔夜政策利率? OPR is the central bank’s policy rate used by banks to set interest rates for loans. OPR是马来西亚银行设定贷款利率的指南。 The OPR is determined by Bank Negara Malaysia (BNM) on a variety of factors and serves as a guide for local banks to determine their own lending rates, both to each other and to the consumer, so cut of OPR will of course bring pros and cons to consumer. It is used to manage the supply and demand for money in the market and forms the backbone of monetary policy. 就是一家金融机构利用手头上充裕的资金借出给另一家金融机构的短期贷款利率(通常是隔夜计算),而这种利率只在各金融机构里互相流通。 Everyone especially households and business owners are waiting to see if Bank Negara Malaysia at its Monetary Policy Committee (MPC) meeting today will trim OPR further to stimulate growth in current economic tough times. Well, lower interest rates will ease the debt burdens on companies and consumers. It is not surprising when BNM announce the cut of OPR today, mark our Bank Negara Malaysia’s 4th policy easing this year, a period in which the economy has faced a triple whammy of coronavirus pandemic, low oil prices and political uncertainty. What about other country?

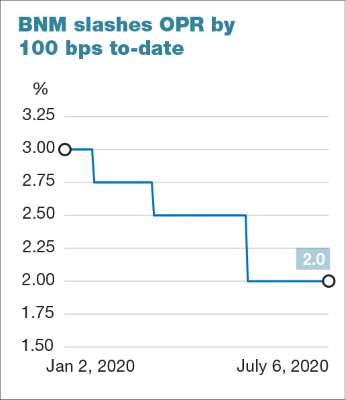

I did a overview of the interest rate cut this year as below.

Source:

The Cut is Good for Country's economy According to The STAR on 7 July 2020, the decision to reduce the OPR is aimed at accelerating the rate of recovery and further stimulate the country's economy. Another way it means to help the economy recover because it supports consumption and investment spending. "The government believes that this move, combined with proactive measures deployed since March 2020 under the PRIHATIN and PRIHATIN SME+ economic stimulus packages and, more recently the National Economic Recovery Plan (PENJANA), will be able to regenerate the economy by creating jobs, restoring consumer and investor confidence, as well as containing the likelihood of a sharp economic contraction,

Savers looking for more returns on their savings accounts and fixed deposits will be disappointed. I I believe further interest rates for these savings instruments will be reduced in tandem with the OPR cut. Advice: We must re-assess our savings or investment strategy to ensure we still get the most optimal returns.

The Lower OPR means you are now able to obtain loans from the bank at a lower rate. Borrowers of flexible interest rate loans will enjoy lower loan servicing payments once banks adjust their base lending rates. A number of banks have since adjusted their rates. I take one example: 1. If you took a personal five-year loan of RM50,000 at 7% interest, with the OPR cut you will be paying RM20 less in monthly instalments. 2. For a 30-year mortgage loan of RM300,000, the monthly instalment is reduced by about RM100 if the bank’s interest rate is reduced correspondingly from 4.5% to 4.0.

Lower borrowing costs would encourage businesses and households, particularly those with good credit scores, to consider taking on new loans.

People will slowly transfer out their savings due to the lower savings/FD rates and put in investment which can provide higher return. When people started to invest in stocks market will help to stimulate economy's growth.

Malaysia ringgit’s weakening also means that goods from overseas will be more expensive. This can potentially affect the country’s economic growth, as many of Malaysia’s projects designed to spur growth are dependent on imports such as highly sophisticated machinery, construction materials, foreign consultant services etc.

OPR reduced will weaken Malaysia Ringgit also. As the weaker ringgit means Malaysian goods will be relatively cheaper compared to their competitors worldwide. Hence, the increased exports should therefore increase output and investment in local enterprises, increasing the opportunities for employment for you and me. Conclusion:When the country experiences strong economic growth, the central bank will consider higher OPRs to discourage overspending as the latter might lead to increased inflation for the country as a whole. The higher lending rates that come with increased OPRs will also mean higher interest rates that attract savings in the banks, discourage indiscriminate borrowing and encourages responsible spending. Alternatively, when the economy is generally found to be slowing the central bank will then consider lower OPR bands to encourage domestic spending, and help GDP growth. This has been used effectively in large economies to spur economic growth, for example in the US, where rates reach 0% with direct liquidity injections conducted through quantitative easing to support the local economy.  Is there an alternative for FD/savings account?

1. Do you want an investment that offers a steady cash flow & yet provide stability (lower risk fund) ? 2. Do you have any Fixed deposit going to due? 3. Do you put all your savings in bank/FD? 4. Do you aware with the lower saving/FD rates offered by bank after the 4th cut in OPR?  For your info:

隔夜政策利率 OPR - Overnight Policy Rate 的由来? 马来西亚国家银行在2004年引用银行隔夜政策利率(Overnight Policy Rate ,OPR)为政府货币政策和管制市场游资的新指标,其用意旨在加强银行体系的良性竞争,为经济带来正面影响。 马来西亚的隔夜政策利率相当于美国的贴现率,是国家银行贷款给商业银行的政策利率;因此,隔夜政策利率的水平,也间接决定了银行发给存款人的利息及贷款利息水平。国家银行让个别银行自定贷款利率,但控制存款利率,可确保存户取得实际的正面回酬,不会受银行利率赚幅压缩的影响。根据国家银行的说法,选定OPR为指标利率,主要是此指标利率相对较稳定,国银仍可通过此利率调控货币政策。在这个利率架构下,如果国银调高OPR,即是紧缩货币政策,反之,就是放宽,整体政策更具透明度。 从此以后,OPR 就成了马来西亚人民最关注的利率指标之一。

0 Comments

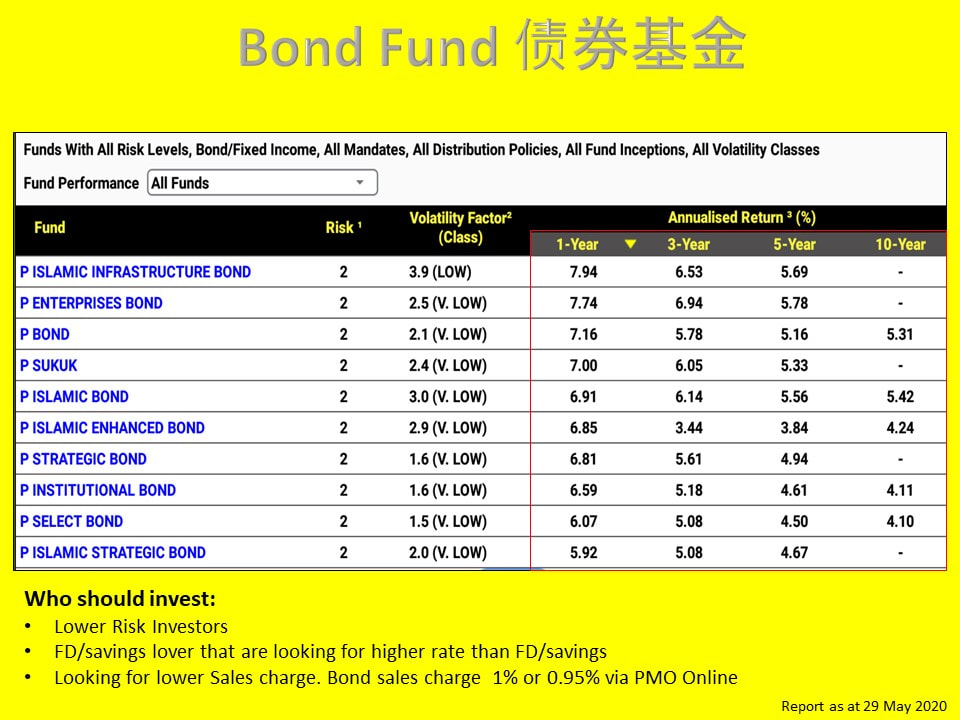

I'm glad that we have the opportunities in China 'A' Share.- Public China Access Equity Fund. Our china funds are mainly invested in 'H' Share all this while for intance: Public Greater China Fund, Public China Ittikal Fund, Public China Titan Fund. I want to highlight one thing here: so basically, Public China Access Equity Fund Concentrated in large-capitalization stocks listed on the China A-share market whereas Public Mutual’ s Other China Funds Largely focus on H-shares market & Also invest in Hong Kong and Taiwan stocks. What you think about 'A' Share fund? some differences between 'A' Share vs 'H' ShareWhat is the differences between 'A' Share and 'H' Share?China incorporated companies listed in the People’s Republic of China (PRC) can issue different classes of share depending on where they are listed and which investors are allowed to own them. The classes are A, B and H, which are all renminbi-denominated shares but traded in different currencies, depending on where they are listed. Publicly traded companies in China generally fall under three share categories:

Fund Objective of PCASEFTo achieve capital growth over the medium to long term period by investing in a portfolio of investments in the China market and including China-based companies* listed on domestic and foreign markets.  Below is our China fund comparison:  Who Should Invest? This Fund is suitable for medium to long-term investors who are able to withstand ups and downs of the stock market in pursuit of capital growth. For a better investment result, you need to determine your fund purpose. Don't ever utilise emergency fund to invest into higher risk fund. For emergency fund, we have Cash deposit fund to cater for you.

Fixed deposit remains one of the best conservative ways to save your money due to its PROS guaranteed returns, higher interest rates (compared to conventional savings accounts) and protection by PIDM. Have you notice recent Fixed deposit/savings is lower? Let me share with you the latest Fixed Deposit rate offered by different banks & Its Pros & Cons  What Happens When You Terminate A Fixed Deposit Early? 1) For fixed deposit accounts of 1 – 3 months Question: If your fixed deposit accounts with terms of one month, two month or three month, you premature withdrawal would see you entitle interest rate? No. Question: Even if you opt to make an early withdrawal one day before the maturity date, you still will enjoy interest rate? No, you will not earn a single sen in interest. 2) For fixed deposit accounts of more than 3 months Question: 1. If you opt to initiate a premature withdrawal any time you still entitle interest rate? No. Question: If you opt to initiate a premature withdrawal AFTER three months, you will still earn interests? Yes, but only at half of the interest rate you were offered. In another word, 50% of the interest you’ve earned is retained by the bank as charges for early withdrawal.

In Malaysia, the interest rate decisions are taken by The Central Bank of Malaysia (Bank Negara Malaysia). The official interest rate is the Overnight Policy Rate. What is OPR? Overnight Policy Rate (OPR) is an overnight interest rate set by Bank Negara. This overnight policy rate or interest rate is a rate a borrower bank has to pay to a leading bank for the funds borrowed. Still don't understand? Maybe I explain in this way. You may wonder why a bank would be borrowing from another bank, but you must understand that bank makes money by lending money out and not by keeping money. Thus, bank will lend out as much money as possible in terms of loans, and maintaining the minimal cash as requested by Bank Negara. However, in the event that cash withdrawal exceeded the amount of cash available, the particular bank will need to borrow cash from other banks, and make an interest rate, which is the OPR.

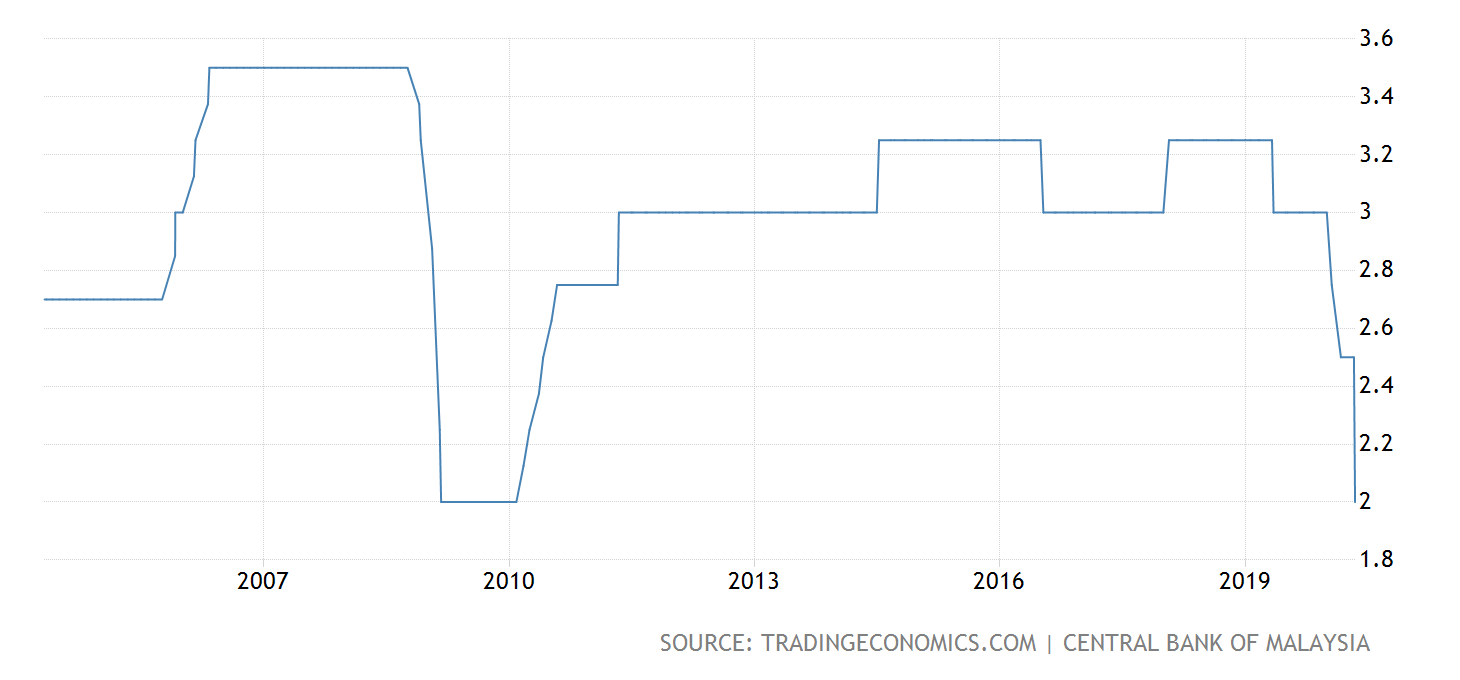

Graph shown the Historical Interest Rate in Malaysia:

https://www.thestar.com.my/business/business-news/2020/07/07/bank-negara-cuts-overnight-policy-rate-by-25bps-to-175  7 JULY 2020: Bank Negara cuts overnight policy rate by 25bps to 1.75% I did a summary of the impact of OPR Cut to the Country & Individual: 1. OPR cut generally positive in impact for businesses and the economy.

2. OPR cut Effect on individual

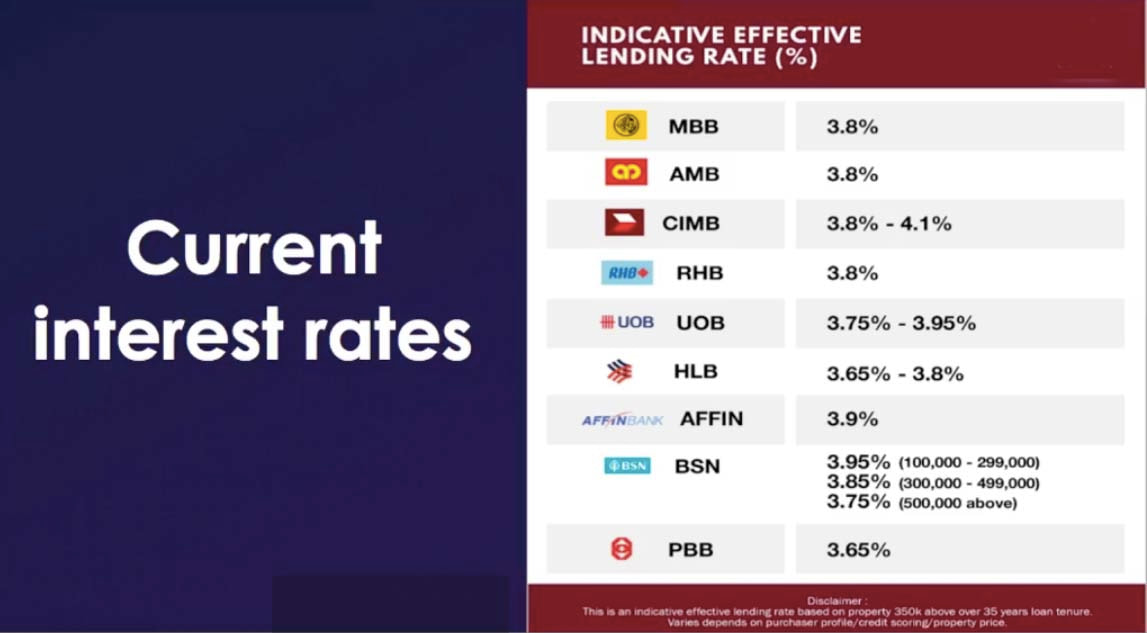

BFR is a rate determined by Islamic banks based on the cost of lending to consumers. (CASH STUDY) Here’s an example of how this works if OPR cut 0.25% Loan amount : RM500,000 Loan tenure: 30 years BR: 3.65% BR: 3.65% – 0.25%= 3.40% Home loan interest rate Before: 4.45% (3.65% + 0.80%) Monthly repayment : RM2,518.59 Total interest paid over 30 years : RM406,693 After OPR cut: 4.20% (3.40% + 0.80%) Monthly repayment: RM2,445.09 Total interest paid over 30 years : RM380,232.40

Latest Housing Loan Interest rate as at March 2020 Below is the latest Fixed Deposit rate after OPR cut as your reference   I would highlight some important point from today The Star. Procrastination is one of the mankind's biggest weaknesses. But in the world of finance, procrastination can result in an opportunity loss to mitigate risk and in growing wealth – sometimes an opportunity which can never be recovered. After all, it takes time for any investment to compound into a significant figure Highlight some of the common reasons people use to put off taking actions on their financial matters.

Advice: What you need to do: Take a long hard look at your expenses. This is critical since we are now in challenging economic times. Mindfully track your spending habits for a month and cut back on luxuries that you can live without. If it helps, set up a standing instruction with your bank to automatically transfer a portion of your salary into another bank account. Use that to start investing. Every small portion helps, so don’t think that cutting back on a small luxury is insignificant.

|

|||||||||||||||||||||||||||||||||||||||